By

By

In the first part of this article we saw that building a sound budget firstly means building a strong relationship with all project partners. A trustworthy relationship with partners will provide a clear and reliable vision since the beginning of roles, costs and needed resources.

In this second part we will analyse the type of costs that all projects include, what are the main pitfalls to avoid and how to interpret the concept of “best value for money”, one of the most important principles stressed by European Commission.

Type of costs

Personnel

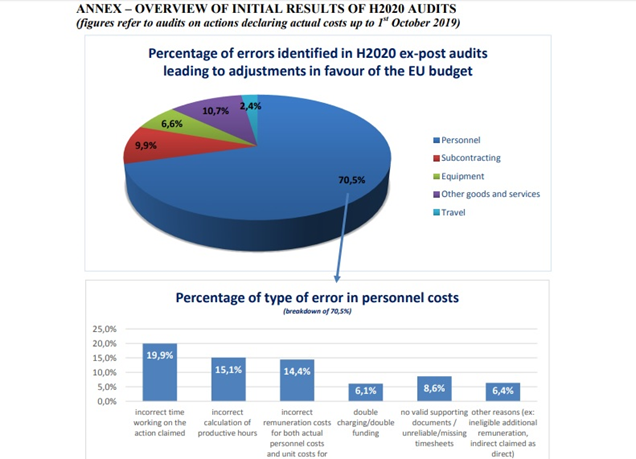

Human resources usually take up the largest part of a project’s budget. To calculate personnel costs, you should usually provide the average monthly cost of staff employed by each partner and the allocation of person-month for each activity and/or WP. As there are many variables to consider (national rules, type of contracts, roles, salaries, etc.), this is the most common category for potential mistakes and errors (up to 70 % of mistakes according to a recent audit in H2020).

As we can see from the table above, half of the mistakes on personnel costs come from an incorrect calculation of time, productive hours and remuneration costs.

All the information about these calculations can be found in the Call’s financial guidelines, but in general, you should calculate the hourly rate of each person employed in the project and multiply the hourly rate by the number of hours they work on the project, documented by a time-recording system.

Remember that with the same PM amount, you can use more of fewer people, according to the time spent on the assigned activity or task.

For example, let’s say that you are a university managing a research activity in a specific WP for a project lasting 24 months. You can choose to involve:

- 3 employees: 1 full time (1), 1 part time (0,5) and 1 with 2 hours/day (0,25)

1 + 0.5 + 0.25 = 1.75 PM x 24 months = 42 PM - 4 employees: 3 part time (0,5 x 3) and 1 with 2 hours/day (0.25)

1.5 + 0.25 = 1.75 PM x 24 months = 42 PM - 5 employees: 1 full time, 3 with 2 hours/day (0.25 x 3)

1 + 0.75 = 1.75 PM x 24 months = 42 PM

Travel, equipment and other direct costs

All goods and resources necessary to carry out tasks and activities constitute other direct costs.

These costs are easier to calculate, as they mainly consist of flights and other transport, accommodation, equipment, services and infrastructure to be used, materials, publications, consumables, documents for dissemination activities. In order to be reimbursed, all these expenses must be incurred, identifiable, verifiable and recorded in the accounts.

It is important to highlight that these costs are linked with their use during the project lifetime. Therefore, if you need to buy a computer, for example, keep in mind that you can only get refunded for its depreciation during the months of the project. When preparing the budget, it is also a good idea to slightly overestimate equipment prices by + 1-2%, considering possible inflation over time. Be careful also about VAT costs which are non-eligible unless they are non-deductible.

Subcontracting

Once all your personnel costs are settled and you have a clear vision of all the resources you will use for the project’s activities, you and your partners can focus on small limited tasks, or highly/specific technical expertise that cannot be covered by anyone in the partnership and should be delegated to an external subcontractor (e.g. a specialized service in a clinical trial, technical assistance to develop the project website infrastructure, support for administrative coordination).

Considering that the EC prioritizes the best value for money, using subcontractors is only recommended if absolutely necessary and should not cover more than 10-15% of the budget (aside from specific and well-explained exceptions).

Remember that you don’t need to specify the names of the subcontractors when submitting the proposal, but you do have to specifically indicate their roles, tasks and costs. Remember that subcontractors are also excluded from the calculation of indirect costs.

Indirect costs

Indirect costs are overheads calculated as a specific flat rate (usually between 7 and 25%) over the direct costs. These can include maintenance, photocopying, telephone, internet and fax costs, heating, electricity or other forms of energy, water, office equipment, insurance and any other expenditure required to successfully complete the project. Indirect costs do not need supporting evidence (accounting documentation).

Project lifetime and cost-effectiveness: two key-concepts

The EC finances all activities carried out during the project lifetime.

It seems quite obvious, but it is important to stress this concept.

In other words, only goods, services and activities which are invoiced and paid by the beneficiaries during the project can be reimbursed.

This means, for example, that if you want to share a study or publication after the end of the project, all costs for printing and dissemination will not be eligible. Two exceptions are constituted by:

- the kick-off meeting which every project must have before it starts. Transport and accommodation costs are usually considered eligible even if paid for before the project’s official starting date

- costs of the audit and final report

The EC always looks for the “best value for money”…

Try to find the right proportions among partners and focus on high cost-effectiveness. If you need to subcontract, ask for at least 3 offers before choosing the supplier that will provide a certain good or service and, if possible, show evidence of these offers in the proposal.

…and good projects – not cheap ones.

You should not aim to draft a low budget as this approach can backfire. All this does is demonstrate a poor assessment and underestimation of the resources you will need to use and make implementing the project unrealistic. On the other hand, focus on the most efficient way to reach the expected results.

Make your cost choices obvious: think horizontally and explain throughout the proposal the reasons you want to use specific activities, countries and methods.

As variables and changes may occur, remember that the budget can be modified and updated even during the project implementation.

To sum up

The devil is in the details. To build a sound budget is like playing chess, you need to estimate the contribution of each available resource and how to move it to achieve the best possible result. For this, you should foster a combined effort of every partner and perform a realistic and well-balanced cost-analysis considering even the smallest details.

This work is long and has many hurdles but, if done well, provides an exceptional solid grounding for the project to run smoothly and increases the chances of overcoming difficulties and unexpected events easily during implementation.

Share: